As a manager, director, or Vice President, you simply must understand the basics of company profitability to be taken seriously.

A Complete Beginners guide to a Profit & Loss Statement (also called Income Statement)

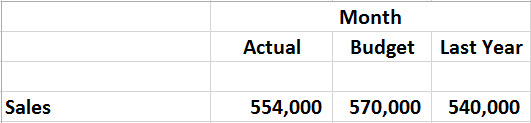

When looking at your company’s management accounts (financial statements); the first thing to look for is how the actual performance compares with the budget and last years performance. You will probably want to drill down into the detail customers making up the total and compare this detail with the detail budget and last year’s total. As you can see from the figures below; the actual is better than last year, but lower than the budgeted figure.

As well as looking at the month, you should also look at the cumulative, in this case below, 4 months cumulative.

Having looked and question the sales figure, we turn our attention to the direct costs, which are:

- Purchases

- Stock movements

- Direct Labour

- Outside contractors

- Any other cost that is directly related to the sale

Sales less direct costs = the Gross Profit. This is an important percentage number, because it tells you how much extra profit you are likely to get or lose by the one extra, or lost sale, because the overheads are in the short-turn fixed in nature.

You can see below that the profitability in numbers and percentage has risen since last year and the short-fall from budget is mainly down to lower than expected sales.

Overheads are made up of anything that is not deemed as direct expenses, such as sales, marketing, accounting, management etc.

Take the overheads from the gross profit to get to the Net Profit before tax, also called Operating Income

In practise the overheads will be shown in much more detail, line-by-line analysis.

This shows that in spite of a good gross profit, the company’s overheads is higher than expected in the budget, more analysis is required